Startup tax.Startup speed.

Tax & books, handled end-to-end. AI agents do the work; a licensed CPA makes the call, in hours, not weeks.

Tax & books, handled end-to-end. AI agents do the work; a licensed CPA makes the call, in hours, not weeks.

Every founder needs two things: speed, and someone who actually makes the call. You get both, so the decisions that move money get made right, in hours.

Receipts, reconciliations, deadlines: AI agents handle all of it in the background. You spend zero hours on tax admin, and nothing slips through the cracks.

See what runs itselfQSBS, entity choice, cross-border: a licensed CPA reads your whole picture and gives you a clear call in hours, not weeks. Reviewed and signed, personally.

Talk to your CPAWe plan all year, not just in April, so QSBS, multi-entity and cross-border savings compound instead of slipping away. That's real runway back in the business.

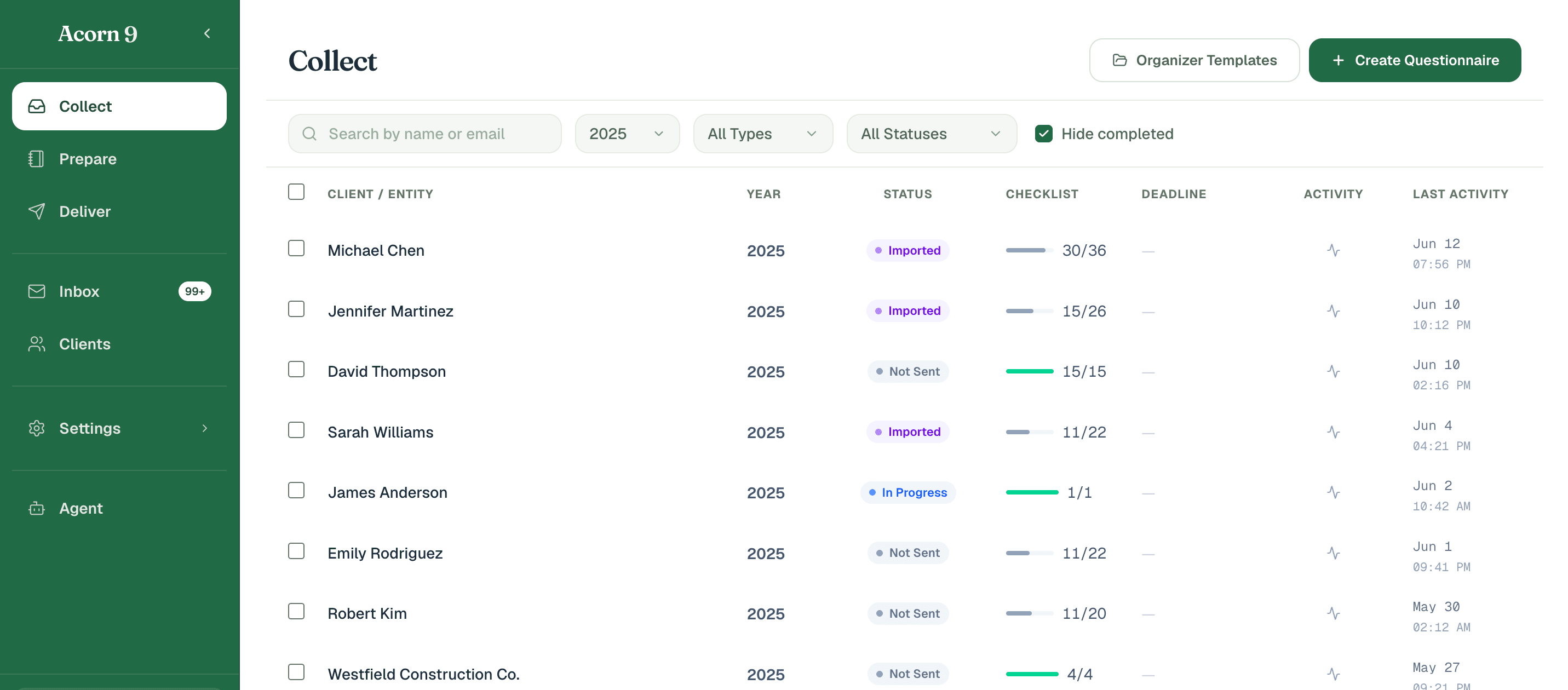

See what we handleSo do the entities around them. Many sit across two. Book one call and we'll sort the structure with you.

From incorporation to year-end filing, six lines of work each run on a clear schedule, so you always know what's done, what's due, and exactly what you get.

These aren't just forms. They're where a complex case gets expensive. We file them every week.

Miss one and it's $10K–$25K, automatic, and it stacks every year nobody filed.

The timing window matters: once it closes, the treatment is often irreversible.

Every new state you touch is another rulebook: Wayfair, registration, ongoing filings.

Late penalties are mostly flat. They accrue whether or not a CPA is looking. These are real, and they stack.

Foreign-owned U.S. entity that didn't file. Each year is another $25K.

U.S. person with foreign-company ownership and no information return.

Foreign accounts over $10K not reported on FinCEN 114.

Plus failure-to-pay, plus interest. The total stacks quickly.

Most cases turned around in 5–10 days once we have your documents.

Real client feedback, each paired with the outcome we delivered.

They'd read everything before our first call. I didn't have to explain my cap table twice, and they kept my QSBS intact straight through the move.

Three LLCs and two mortgages. I couldn't tell which entity reported what. They mapped the whole structure for me and got it lender-ready.

Nobody owned sales tax, payroll, or the overseas parent. They took the whole picture. Now the U.S. tax side just runs while we open stores.

15 minutes with a licensed CPA. No sales pitch, just straight answers on the entities, deadlines, and decisions other firms punt on.

A licensed CPA will reply within 1 business day with your private folder and next steps.